Most developers evaluating the UAE still begin with Dubai. That instinct is understandable, but Abu Dhabi’s property market now warrants much closer attention. The market crossed AED 142 billion in transactions in 2025, and the bigger story is not just the scale of growth, but where that growth is concentrated and how quickly the opportunity set is evolving for new entrants.

Residential demand continues to outpace supply, sustaining price pressure across multiple segments. This Abu Dhabi real estate market overview examines what is driving that momentum, which micro-markets deserve closer evaluation, and how the 2025 regulatory reforms could shape your next project.

The Abu Dhabi real estate market recorded 42,814 transactions in 2025, a 52% jump in deal count alongside a 44% rise in total value, according to the Abu Dhabi Media Office. Residential sales alone reached AED 76.1 billion across 23,600 transactions. Apartment sale prices rose 19%, villa prices climbed 13%, and rental yields in designated investment zones increased by 14%.

Residential demand is growing quickly. The absorption of new supply alongside rising prices suggests demand is not purely speculative, although segment-level overheating risks may still appear in premium zones. Population is expanding, the non-oil economy is strengthening, and commercial real estate is operating with limited slack.

Taken together, those conditions are reinforcing residential demand in ways that are likely to remain relevant over the medium term. For developers assessing timing, product mix, and compliance strategy to target the residential development market, an experienced project and development partner like TPI can reduce early execution risk.

Understanding what’s sustaining the Abu Dhabi real estate market requires looking beyond transaction data to the underlying economic conditions that generate demand.

1. Population Growth Is Widening the End-User Base

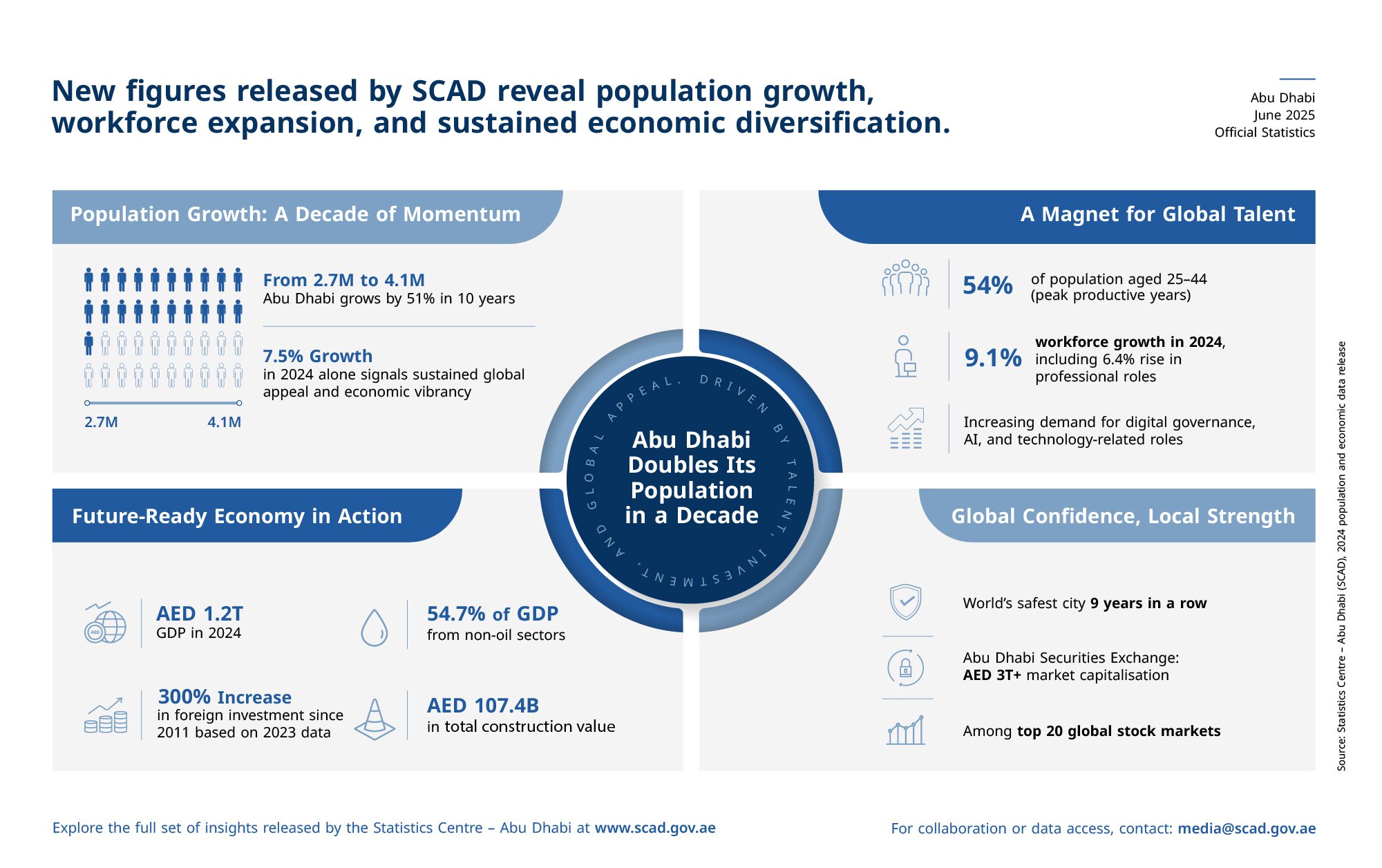

Population growth is the clearest starting point. Abu Dhabi’s population expanded 7.5% in 2024, creating a broader base of residential end-users. For developers, this points to rising demand for mid-income and family-oriented housing, not only investor-led inventory.

2. The Non-Oil Economy Is Supporting Housing Demand

The non-oil economy is expanding at a pace that is feeding directly into job creation and household formation. Sustained office occupancy at 97% also signals stable business activity and deeper end-user demand, reducing dependence on short-term investor sentiment alone.

3. Infrastructure Spending Is Reshaping Future Value

Abu Dhabi’s infrastructure pipeline is another major factor. Disneyland Abu Dhabi, the Guggenheim Museum, and expanded convention facilities are funded and under construction. These projects are not only headline investments. They also function as land-value multipliers, particularly in areas such as Yas and Saadiyat, where developers may be positioning projects ahead of future infrastructure-led appreciation.

4. Market Conditions Still Favour Well-Timed Launches

Current conditions continue to support project launches with the right product-market fit. Demand remains healthy, active zones are seeing strong pre-sales activity, and buyers are responding to locations with a clear lifestyle or investment proposition. That window may not stay open once more supply reaches the market, which is why timing discipline matters.

TPI’s role in this stage is often less about broad market commentary and more about helping developers translate these signals into practical decisions around phasing, budgeting, positioning, and delivery strategy.

TPI’s role in this stage is often less about broad market commentary and more about helping developers translate these signals into practical decisions around phasing, budgeting, positioning, and delivery strategy.

The strongest returns are not spread evenly across Abu Dhabi. Developers need to evaluate each micro-market based on buyer profile, proximity to infrastructure, pre-sales depth, and long-term exit potential.

Off-Plan Has Become the Default Transaction Type

Off-plan transactions now account for the majority of residential deals. That is not simply a matter of buyer preference. It reflects a broader market shift in which investors are willing to commit earlier because Abu Dhabi’s off-plan projects have historically shown capital appreciation, and current pre-sales conditions remain healthy in active zones.

For developers, this matters because strong early absorption can improve revenue visibility before construction costs rise.

The Most Active Zones Are Serving Different Strategies

The most active development zones currently include Yas Island, Saadiyat Island, Hudayriyat Island, and Fahid Island. Each serves a different buyer profile, but all four benefit from strong infrastructure linkages and sustained investor attention.

How to Choose:

Rental Yield Profiles by Area

Abu Dhabi rental yields are approaching 9–10% in areas like Al Ghadeer, but developers should expect compression as capital values rise over the next 12–24 months. The 2026 real market price appreciation will push yields down in premium zones.

That is why launch timing is important. Developers entering now may still be able to access a more favourable price-to-yield ratio than those who wait for a more crowded phase of the cycle.

Affordable Housing Is Where the Supply Gap Is Sharpest

The most underbuilt segment in Abu Dhabi right now is not luxury housing. It is mid-income housing. Developers that remain concentrated in premium inventory are competing in tighter spaces, while areas such as Baniyas and Khalifa City appear to remain structurally underserved.

Government housing initiatives have also created partnership opportunities for private developers in this segment. Competition from players such as Aldar and Modon is generally less intense here than in premium-led corridors, and the entry economics on land can be more accessible.

For developers evaluating scale, absorption, and downside protection, this segment may deserve more attention than it typically receives.

The regulatory environment is where many international developers underestimate what they’re walking into, and 2025 brought meaningful changes worth mapping before committing capital.

ADREC, the Abu Dhabi Real Estate Centre, introduced a triple-protection framework effective August 2, 2025, creating new legal protections for developers, purchasers, and financiers across the entire project lifecycle. For developers, this shifts the model away from heavily sales-funded construction toward a more finance-backed structure, which has direct implications for capital planning.

The escrow requirement is the piece that most directly affects your cash flow planning. Buyer payments on off-plan projects go into regulated accounts, with disbursements tied to verified construction milestones. Developers cannot rely on those sales proceeds to fund earlier phases of construction. Bridge finance and construction facilities, therefore, need to be structured independently of the timing of off-plan collection.

Freehold zone expansion is the other major 2025 development, with new areas now open for 100% foreign ownership. Given that investors from Russia, China, the UK, and the US are among the most active buyers in the Abu Dhabi real estate market, this reform materially expands the addressable pool of buyers.

Developers can review the current framework through ADREC’s official rules and regulations portal.

This is another point where early advisory support matters. Regulatory clarity helps, but execution still depends on sequencing approvals, financing, delivery controls, and buyer-facing credibility in the right order.

For developers, the Abu Dhabi opportunity is no longer just about participating in a growing market. It is about making disciplined decisions on launch timing, product positioning, buyer targeting, and compliance structure while conditions remain supportive. The developers most likely to perform well in this cycle will be those who treat market entry as a strategic exercise, not simply a land acquisition or sales decision.

1. Launch Timing Can Directly Influence Absorption and Pricing Power

For developers, timing is not just a scheduling issue. It can materially affect pre-sales momentum, buyer response, and margin protection. Projects launched within the current window may benefit from stronger absorption conditions, while those delayed by 6 to 12 months could enter a more crowded supply environment with less pricing flexibility.

2. Product Strategy Should Align With Actual Demand Depth

Developers need to look beyond headline price growth and assess where demand is deepest and most sustainable. A pipeline weighted entirely toward luxury products may limit exposure to a narrower buyer base. At the same time, a more balanced mix of premium and mid-income offerings can improve absorption, diversify revenue, and reduce concentration risk across the portfolio.

3. Compliance Can Support Both Execution and Marketability

For developers, regulatory readiness is not only about approvals and process. It also has commercial value. Escrow compliance, ADREC licensing, and a clearly structured project framework can strengthen buyer confidence, particularly among international investors who often use regulatory discipline as a proxy for delivery credibility.

4. Buyer Strategy Should Reflect the Differences Across Foreign Investor Groups

Developers targeting international demand should avoid treating overseas buyers as a single market. Investors from Russia, China, the UK, and the US often differ in capital priorities, documentation expectations, financing preferences, and risk tolerance. A more segmented go-to-market strategy can improve buyer conversion and support more efficient sales planning.

5. Mixed-Use Developers Should Track Commercial Demand Closely

For developers pursuing mixed-use opportunities, commercial leasing conditions can offer an important read on the project’s broader strength. Healthier performance on the commercial side can support faster stabilisation, improve asset quality, and strengthen the overall investment case for integrated developments.

Abu Dhabi’s property market is not being driven solely by sentiment. The demand-supply gap, the increase in foreign capital, the regulatory clarity introduced through ADREC’s 2025 reforms, and the infrastructure pipeline all point to structural drivers with multi-year relevance.

Developers that enter with clear positioning, disciplined financing, and a realistic understanding of underserved segments are more likely to find durable opportunities here.

If you are evaluating a project in Abu Dhabi, TPI can support you as a strategic development and project management partner, helping you assess feasibility, align delivery plans, and move from market opportunity to execution with greater confidence.

1. Is Now a Good Time for Foreign Developers to Enter the Abu Dhabi Property Market?

The Abu Dhabi real estate market has seen a 363% increase in foreign investment since 2022, as per ADREC’s official market data, reflecting genuine confidence from international capital rather than speculative interest. ADREC’s 2025 reforms have considerably reduced legal ambiguity, and the freehold zone expansion now allows 100% foreign ownership across more areas than before.

2. What Rental Yields Should Developers Target in Abu Dhabi?

Rental yields across the Abu Dhabi real estate markets are rising. These yields coexist with capital appreciation in most investment zones. Developers building investor-buyer products should model both income yield and resale value at handover, since that combination is what’s driving buyer decisions in the current market.

3. How Does ADREC’s Escrow Requirement Affect Project Financing?

ADREC’s escrow requirement means buyer payments for off-plan projects are held in regulated accounts until verified construction milestones are met, as detailed in ADREC’s rules and regulations. Developers can’t use those proceeds to fund earlier phases of construction.

4. Which Micro-Markets Are Producing the Strongest Off-Plan Sales Right Now?

The most active off-plan zones in the Abu Dhabi real estate market right now are Yas Island, Saadiyat Island, Hudayriyat Island, and Fahid Island, all showing strong pre-sales conditions driven by proximity to infrastructure and freehold ownership frameworks.

For developers targeting mid-income demand, with less competition from government-backed developers, Al Reem Island, Al Ghadeer, and Khalifa City are showing solid buyer interest, with more accessible entry economics on land and site acquisition. The right zone depends on your product type, target buyer profile, and financing structure.

5. How Does Abu Dhabi Compare to Dubai for Property Development Opportunities?

Abu Dhabi’s property market is less mature than Dubai’s in terms of development cycles, creating genuine opportunities in segments that Dubai has already absorbed. Rental yields in comparable Abu Dhabi zones tend to be higher than those in Dubai, and the market is showing resilience even amid global uncertainty.

Dubai has stronger global brand recognition, but Abu Dhabi’s infrastructure commitments, demand-supply dynamics, and a diversifying international buyer base make it increasingly compelling for developers with a three- to five-year project horizon.